When the NAR settlement took effect on August 17, 2024, the industry’s loudest voices had a clear prediction. Mandatory buyer-agent compensation was over. Buyers would represent themselves or negotiate fees down to nothing. TD Cowen analysts projected a 25 to 50 percent decline in overall commission rates. HousingWire ran pieces on commission compression. The consensus was that real estate had finally hit the moment it had been bracing for: the beginning of the end for traditional compensation structures.

That is not what happened.

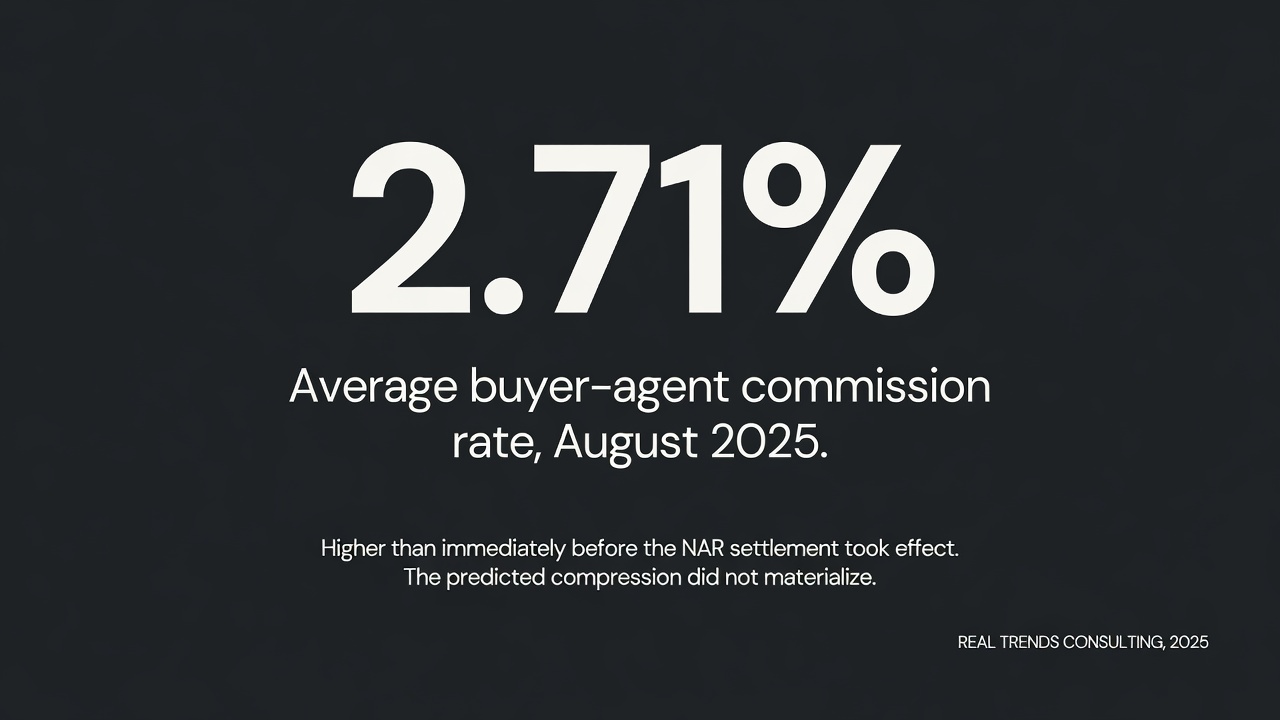

Buyer-agent commission rates dipped in the immediate aftermath of implementation, then reversed. By August 2025, RealTrends Consulting data showed average buyer-agent commissions at 2.71%, up from 2.65% immediately before the settlement took effect. Among homes under $500,000, Redfin transaction data showed rates at their highest point since 2023. The rebound was documented by Redfin, RealTrends, and AccountTECH across hundreds of thousands of transactions. It held across geographies. It held across price tiers below the luxury segment.

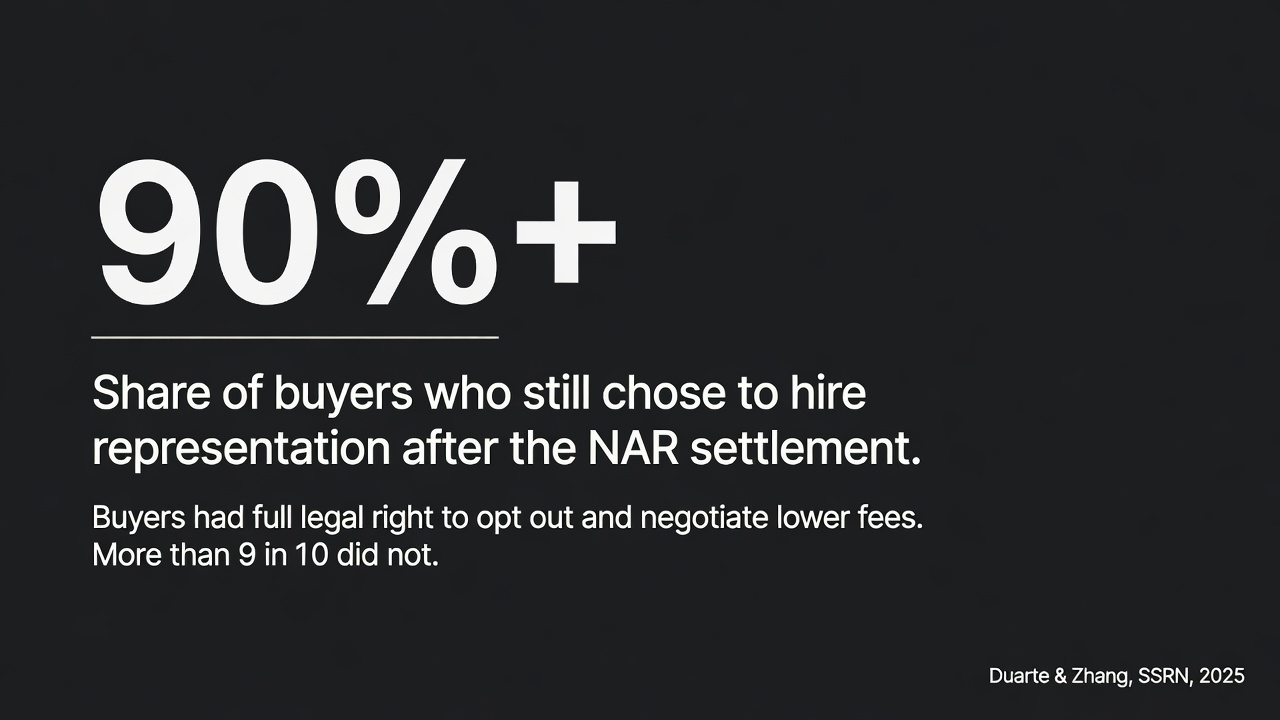

More telling than the rate data: more than 90 percent of buyers still chose to hire representation post-settlement, according to research by Duarte and Zhang published through SSRN. Buyers had more information than ever about what they were paying and why. They had the legal right to negotiate. They had the structural ability to opt out entirely. More than 90 percent of them did not.

That is a verdict.

The conventional analysis of commission rates asks the wrong question. It asks what consumers will pay when forced to pay explicitly and transparently. The settlement provided the answer. They paid the same rate they paid before, or close to it. They did not bolt. They did not represent themselves in meaningful numbers. They looked at a transaction full of contingencies, counterparties, inspections, financing conditions, and compressed timelines, and decided that the professional sitting across the table from them was worth paying.

The industry has been telling a defensive story about this for two years. The instinct has been to justify, to explain, to argue that commissions were always earned. That instinct is wrong. Defensive arguments about value are made by people who are not sure they have it. The data does not require defense. It requires interpretation.

What consumers were buying when they hired and paid a buyer’s agent is not complicated. They were buying three things that no automated system has figured out how to replicate: a street-level understanding of what the market is actually doing, the ability to navigate a complex set of relationships with sellers, listing agents, lenders, and inspectors who all have their own objectives, and the capacity to evaluate a property not just by what comparable sales say it is worth today but by what neighborhood dynamics, home type trajectory, and larger market forces say it will be worth in the future. These are judgment-intensive, relationship-intensive, context-intensive competencies. They are what the consumer is paying for. The settlement made that explicit.

The rebound is not uniformly good news, and what the data shows underneath the headline number deserves attention. Commission rates in the luxury segment continued to compress throughout 2025. The buyers most capable of representing themselves (high net worth, high transaction experience, well-advised) did negotiate lower fees or chose not to hire representation. The consumers who kept paying for agents at or above prior rates were concentrated in the under-$500K segment: first-time buyers, less experienced negotiators, buyers whose transactions were most complex relative to their experience.

The market did not validate every agent. It validated the agents who could demonstrate real accountability, real expertise, and real stakes on behalf of their clients. The ones who couldn’t lost ground to the pressure the settlement created. The rebound is not a reprieve for the profession. It is a sorting mechanism.

Agents who understand this will stop treating the settlement as something to survive and start treating it as the clearest possible market signal about what justifies their existence. The industry spent years avoiding a transparency it did not want. The transparency arrived. The consumers who could have punished them for it chose not to.

That should end the apology tour.